From Defined Pension to Assured Pension

Dheeraj Jandial

Blending the key features of the Old Pension Scheme (OPS) and the National Pension System (NPS), the Centre Government unveiled Unified Pension Scheme for central government employees. The scheme’s effective date is April 1, 2025. The Union Government has impressed upon the States to look into the implementation of the UPS at the earliest.

Jammu and Kashmir, which presently has an elected government too shall be deliberating upon the UPS for its employees in the commencing Budget session and it is expected that option shall be provided to the employees to either switch to the UPS or continue in the NPS. As per conservative estimates, if all States opt for implementation of UPS then the number of employees benefitting from scheme is likely to surge to 9 million.

Lauding the introduction of Unified Pension Scheme, the Prime Minister Narendra Modi emphasised its role in securing the financial future of government employees. The Prime Minister said, “We are proud of all the government employees who work hard for the progress of the country. The Unified Pension Scheme (UPS) ensures dignity and financial security for these employees. This step reflects our government’s commitment to their welfare and secure future.”

In fact, pension has always been one of the main lures of a government job. This element of security is one of the primary reasons why a government job is coveted in India. The hike in pension and its quantum addition is always aspired for, as it has direct relation with the mental wellbeing of the pensioners. This aspiration for hike and associated social security could well be narrated in the quote by Mirza Ghalib, haaaron ?hvahishen aisi ki har khvahish pe dam nikle, bahut nikle mire arman lekin phir bhi kam nikle.

WHAT IS U.P.S. ?

The decision to introduce an assured pension for central government employees reflects political pragmatism over strict fiscal calculations.

Approved by the Union Cabinet on August 24 for 2.3 million central government employees across India, the Unified Pension Scheme (UPS) is amalgamation of New Pension Scheme (NPS) and the Old Pension Scheme (OPS). Through the Unified Pension Scheme, the government aims to address the dissatisfaction among employees with the NPS.

The Unified Pension Scheme (UPS) is likely to have significant impacts on government with high debt and a large debt to GDP ratio

As the scheme will be effective from April 1, 2025, all central government employees who retire on or before March 31, 2025, and are entitled to arrears, will be eligible for the Uniform Pension Scheme (UPS). Employees with the National Pension System (NPS), which is applicable to individuals who entered service after April 1, 2004, have the option to select between the two pension schemes.

To transit from NPS to UPS, the employees are required to finalise their decision prior to the scheduled implementation date. Once the choice for UPS is made, it is irrevocable, and a return to NPS is not permissible. The government affirms that over 99% of employees will experience advantageous outcomes through the adoption of the aforementioned new scheme.

The Unified Pension Scheme is still a contributory scheme but the government’s share will be 18.5 per cent and there is an element of assured sum built into it. The salient features of Unified pension Scheme are as under: –

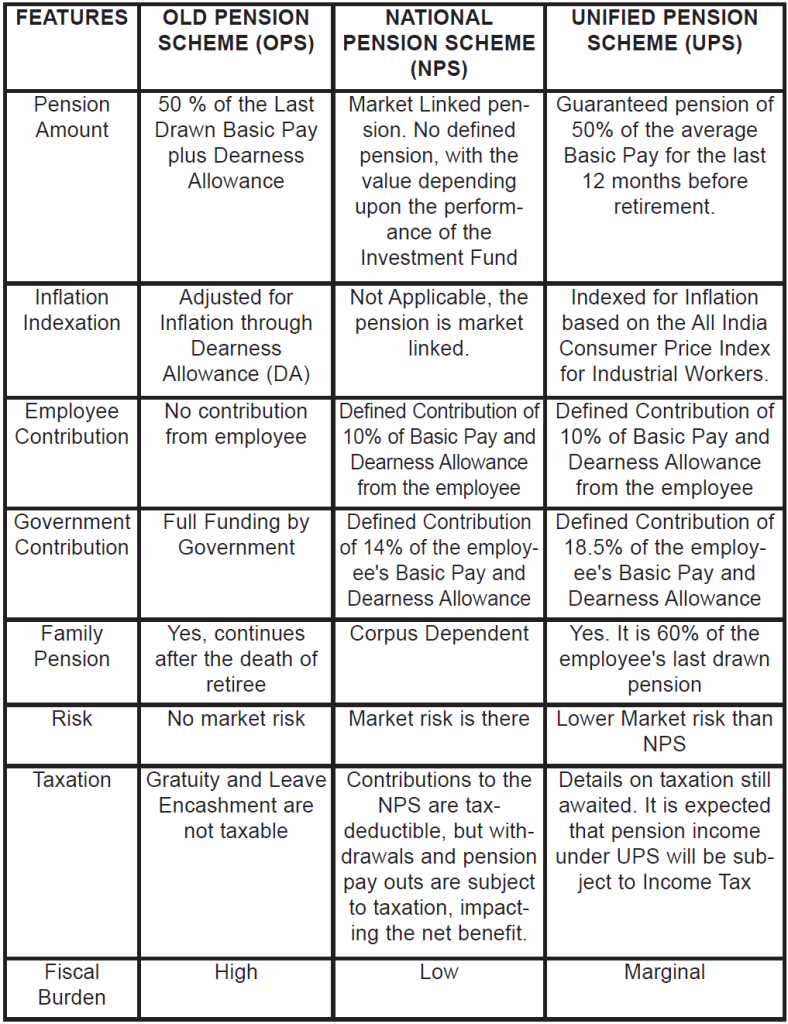

- Retirement income guaranteed-Assured Pension: Under this scheme, retirees will receive a pension amounting to 50 per cent of the average basic pay drawn over the last 12 months prior to retirement, for a minimum qualifying service of 25 years. The pension will be proportionate for those with shorter service periods, with a minimum requirement of 10 years of service.

- Protection of families-Assured Family Pension: If an employee passes away, UPS pays 60 per cent of the deceased’s actual or projected pension to the employee’s surviving family members. The purpose of this provision is to protect the financial security of the dependents.

- Pension cut-off point- Assured Minimum Pension: Regardless of their final salary, pensioners with 10 or more years of service are given a minimum monthly pension of Rs 10,000. This clause creates a basic financial safety net for all retirees and is a crucial differentiator with the NPS.

- Adjustments for cost of living- Inflation Indexation: In order to maintain retirees’ spending power, UPS uses inflation indexation. Pension amounts are routinely adjusted based on the All-India Consumer Price Index for Industrial Workers (AICPI-IW), similar to the Dearness Allowance adjustments for current employees so as to assist retirees in keeping up with rising living expenditures.

- Bonus for retirement- Lump sum Payment: Employees will receive a lump sum payment one time upon superannuation. This bonus will be given in addition to the gratuity and has no bearing on the normal pension amount. This amount is calculated as 1/10th of their last drawn monthly pay (including DA) for every six months of service completed. This payment is separate from the gratuity and does not affect the assured pension. It will provide a financial safety net as you move closer to retirement, says the government.

HOW IS UPS DIFFERENT FROM NPS?

- Jo Dikh Raha Usi Ke Andar Jo Andikha Hai Vo Shaiirii Hai,

- Jo Kah Saka Tha Vo Kah Chuka Huun Jo Rah Gaya Hai Vo Shaairii Hai

The National Pension Scheme (NPS) was a significant development as it marked the initiation of a defined contribution system where both employees and the government contributed to the pension fund at rates of 10% and 14% of the employee’s salary, respectively. The employees’ contributions were directed towards market-linked securities like equities, which meant that the final pension amount was influenced by the performance of these investments. As such, the NPS is more like a savings scheme, almost like a systematic investment plan (SIP), which is exposed to the equities market. It has done well for the beneficiaries, offering an average of 10 per cent annual return. NPS is managed by nine different pension fund managers, including prominent names such as Max Life, ICICI, Tata, SBI, Kotak Mahindra, LIC, Aditya Birla, HDFC, and UTI. These fund managers offer schemes with varying levels of risk, from low to very high, catering to different investment preferences.

Under the NPS Scheme-Central Government, managed by major players like LIC, SBI, and UTI, the returns have been around 9.22 per cent over a 10-year period and so on, according to market data. The high-risk options have even yielded 15 per cent or thereabouts. The instrument has attracted more and more private employees as well. And by now the total asset under management of the NPS has grown to over Rs 12 lakh crore.

But it’s still not assured pension and it still makes government employees expose their savings to market risks-a major bone of contention for employees demanding a scrapping of the NPS. “The only difference in the changes that are made is to give an assurance and not leave things to vagaries of market forces. The structure of UPS has the best elements of both OPS and NPS,” said cabinet secretary-designate T.V. Somanathan while speaking to the media about the Cabinet decision, while introducing the UPS.

THE TRIO- IN COMPARISON

WHICH PENSION SCHEME WILL BE MORE SUSTAINABLE?

The newly approved UPS is designed to strike a balance between the government’s fiscal policy and employee benefits by offering a defined benefit pension similar to the OPS, while maintaining the contributory nature of the NPS. Under the UPS, government employees will receive a guaranteed pension

Pension liabilities are long term in nature. Defined Contribution schemes like NPS put the onus of sustainability of the benefit onto the individual. Sustainability of UPS which is a Defined Benefit, index linked pension liabilities (with an additional family pension) would be very challenging for the government. While the scheme entails setting aside a guaranteed reserve fund to reduce exposure of the government to additional contributions, the investment of these funds has to be monitored tightly through strong governance of the investments.

Whether one should opt for UPS or continue in NPS would really depend upon individual circumstances. UPS has a minimum service requirement, so the younger workforce who would want greater flexibility and mobility may still find NPS more advantageous. For the more tenured employees closer to retirement, UPS would have an obvious advantage. To sum up, the Urdu couplet Halki phulki si hai zindagi, bojh tuo khwaishon ka hai; Aaj maine fir jazbaat bheje, aaj tumne phir alfaaz samjhe, assumingly narrates the pensioners dilemma.

(The writer is District Treasury Officer, Udhampur and can be reached at [email protected])